Del Monte Pacific: Operating Recovery Amid Residual Balance Sheet Strain

Del Monte Pacific Limited delivered a materially improved performance for the second quarter and first half ended 31 October 2025, following the deconsolidation of its U.S. operations effective 1 May 2025. The results reflect a clearer earnings profile and stronger core operations, though balance sheet constraints remain a central consideration.

On the positive side, operating performance strengthened meaningfully. Second-quarter turnover reached US$234.9 million, up 9.9% year-on-year, while first-half revenue grew 11.3% to US$438.6 million. More importantly, profitability improved at a faster pace than revenue. Gross margin expanded from 27.6% to 34.2% in the second quarter and to 33.4% for the first half. The margin expansion was driven by improved pricing discipline, a favorable sales mix anchored on premium fresh exports, lower input costs for tinplate and sugar, and improved cannery efficiency.

Operating profit rose 56.8% in the quarter and 48.1% for the first half, demonstrating operating leverage within the core business. Net profit attributable to shareholders reached US$16.8 million in the second quarter and US$22.3 million for the first half, representing a substantial turnaround from the prior year. EBITDA growth further supports the view that the earnings recovery is operational rather than purely accounting-driven.

Geographically, the Philippine market remained resilient, supported by strong demand for packaged fruits, beverages, and culinary products. Internationally, fresh pineapple exports to China and Japan continued to perform well, with the Group maintaining a 51% share of imported pineapples in North Asia. These trends indicate that the Asian franchise remains structurally intact and competitively positioned.

The deconsolidation of the U.S. operations resulted in the removal of approximately US$1.5 billion in liabilities, improving leverage metrics. Net debt declined to approximately US$994.9 million, and net debt-to-EBITDA improved to 6.1x from 8.3x a year earlier. Operating cash flow remained solid at US$162.7 million for the first half, despite higher inventory levels ahead of peak season.

However, structural risks remain evident. Total equity stood at negative US$591.9 million, and net asset value per share remains negative. While profitability has recovered, the capital deficiency arising from prior impairments continues to weigh on the balance sheet. Leverage, though improved, remains elevated for a consumer staples business, and earnings remain exposed to foreign exchange volatility, tax normalization, and joint venture impairments.

In sum, Del Monte Pacific has transitioned from crisis stabilization to operational recovery. The core business is performing well, margins have expanded, and cash flow generation is stable. Nevertheless, sustained profitability and continued deleveraging will be necessary to restore balance sheet strength and fully normalize the company’s capital structure.

Del Monte Pacific Limited (DELM) Price Structure

On February 25, 2026, Del Monte Pacific Limited (DELM) closed at ₱5.40 per share, up 8%, despite registering net foreign selling of nearly ₱2 million. The ability to advance meaningfully in the presence of foreign outflows suggests that local demand absorbed available supply, reinforcing the short-term bullish tone.

DELM continues to trade above both its 9-day EMA and 200-day EMA, with the shorter-term EMA hovering above the longer-term EMA. This alignment confirms that short-term momentum remains constructive within a broader recovery structure. The positioning of price above both moving averages indicates that buyers maintain control across multiple time horizons.

Technically, DELM has successfully sustained its position above ₱4.93, which corresponds to the 61.8% Fibonacci retracement. This level is critical, as it represents the deeper retracement threshold often associated with trend invalidation if breached. The chart clearly shows repeated defenses of this zone, suggesting that market participants recognize its structural importance.

As long as ₱4.93 holds, the probability of continued upside exploration increases. Failure to defend this level, however, opens the path toward the deeper support band between ₱4.27 (50% retracement) and ₱4.60 (38.2% retracement). That zone would serve as the next structural cushion should momentum weaken.

On the upside, immediate resistance is positioned at ₱6.00, a psychological barrier and prior reaction area. A decisive move above this level would signal expansion beyond the current recovery phase.

Volume behavior strengthens the bullish case. Over the past three consecutive trading days, daily volume exceeded 100% of both the 10-day and 50-day volume averages, indicating sustained participation rather than a one-day spike. Multi-session volume expansion often reflects accumulation rather than short covering.

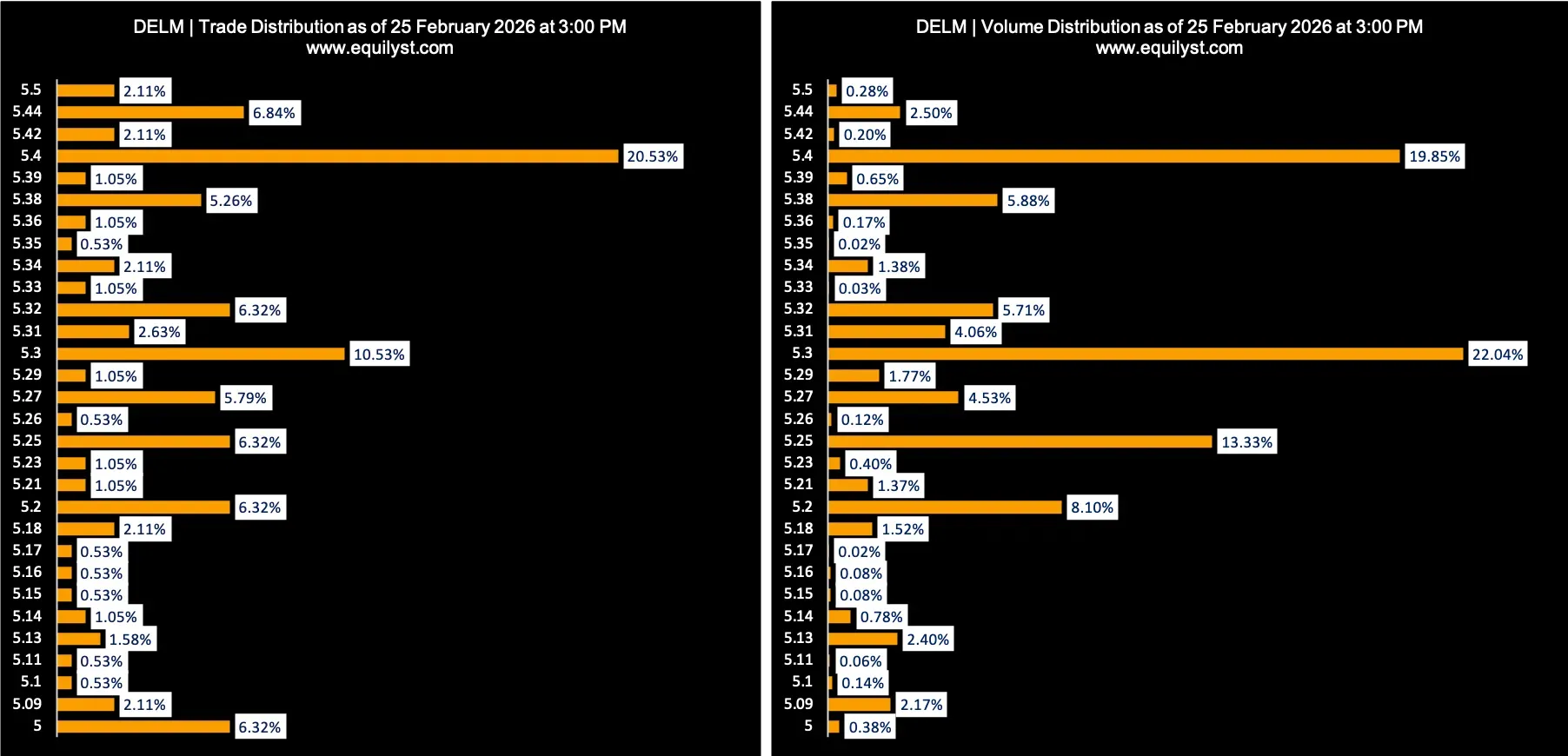

Dominant Range Index: BULLISH

Last Price: 5.40

Dominant Range: 5.30 – 5.40

VWAP: 5.3003

The Dominant Range Index prints BULLISH, with the dominant range positioned at the upper boundary of the session. This suggests that the highest concentration of transactions occurred near the closing level rather than at discounted prices.

Price closing above the VWAP of ₱5.3003 further confirms intraday strength, as participants were willing to transact above the session’s volume-weighted average price. When dominant volume clusters form near highs, it reflects acceptance of higher pricing rather than hesitation.

This positioning supports continuation bias in the near term, provided follow-through demand persists.

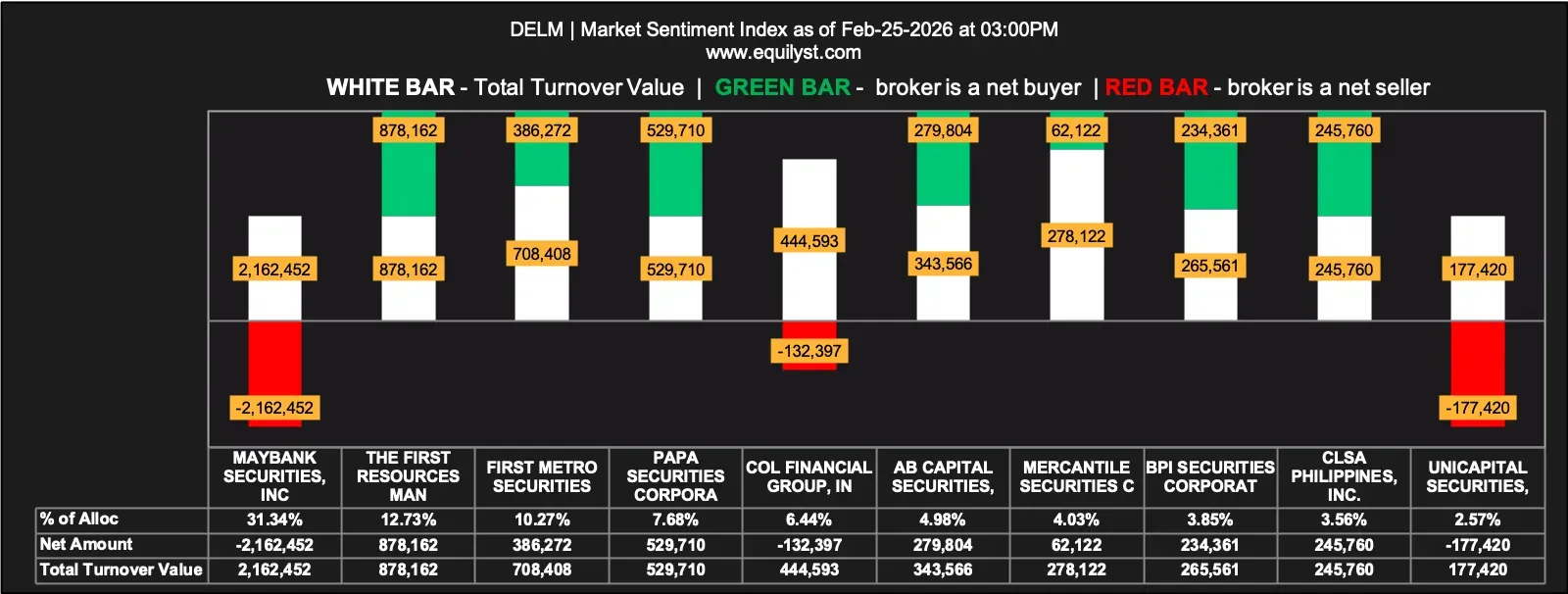

Market Sentiment Index: BEARISH Divergence

14 of 25 participating brokers (56.00%) posted a positive Aggregate Net Amount

12 of 25 participating brokers (48.00%) posted a higher Per-Broker Buying Average than Selling Average

Aggregate Buying Average: ₱5.31993

Aggregate Selling Average: ₱5.31401

9 of 25 participants (36.00%) registered 100% BUYING activity

9 of 25 participants (36.00%) registered 100% SELLING activity

Despite strong price action and a bullish Dominant Range Index, the Market Sentiment Index registers BEARISH, creating a participation divergence beneath the surface.

While a majority of brokers (56%) posted positive aggregate net amounts, the balance between pure buyers and pure sellers is evenly split at 36% each. This symmetry suggests that the advance was met with both conviction buying and active distribution.

Notably, the aggregate buying average is slightly higher than the aggregate selling average, indicating that buyers were willing to transact at marginally higher prices. However, the elevated proportion of 100% selling participants tempers the enthusiasm, implying that supply remains active into strength.

This divergence does not invalidate the bullish structure, but it suggests that the rally is not universally supported across broker participation.

Consolidated Outlook

DELM’s technical structure remains constructive:

- Price trades above both the 9-day and 200-day EMAs

- The 61.8% Fibonacci retracement at ₱4.93 continues to hold

- Volume has expanded for three consecutive sessions

- Dominant range is positioned at session highs

These factors collectively favor upside continuation toward ₱6.00, provided ₱4.93 remains protected.

However, the BEARISH Market Sentiment Index and balanced broker distribution indicate that the move is not yet broad-based. Sustained momentum will likely require continued volume expansion and stronger participation alignment.

For now, DELM maintains a bullish structural bias, but monitoring participation breadth will be essential in determining whether this advance evolves into sustained expansion or stalls into consolidation.

If you want to understand how this setup may unfold in the coming sessions, reach out to us through the contact form below.